Avoiding A Tax Penalty

Table of Contents

- Avoiding A Tax Penalty

- How To Avoid A Tax Penalty When Selling Your Home

- Avoiding Tax Penalties

- Do You Have To Buy A House To Avoid The Tax Penalty

- Do I Have To Pay Capital Gains Tax When I Sell My House?

- 2025 Capital Gains Tax

- Do You Pay Sales Tax On A House? What You Need To Know

- Understanding Capital Gains Tax and How It Affects Home Sales

- Length Of Ownership Matters

- Exclusions

- How To Minimize or Avoid Capital Gains Tax When Selling Your Home

- Can You Avoid Tax Penalties When Selling Your Home?

- Some Exclusions and Exceptions

- What Is The Tax Penalty For Selling A Home?

- Timeframe For Buying A New House To Avoid Tax Penalties After Selling

- The Roll Over Rule Is No More

- IRS-Compliant Reinvestment Strategies

- Tips To Eliminate Or Reduce Tax Penalties On Home Sales

- Advanced Strategies

Avoiding taxes is the American way of life, perfectly legal, and encouraged by the IRS. However, never confuse avoidance and lessening with evasion. The most significant purchase most of us will ever make is our home. Start now to develop effective strategies to avoid tax penalties and deal with capital gains when it is time to sell. It is a mistake to think capital gains can be avoided; other actions can lessen them, but the IRS will get its money. They cannot be dealt away.

Profiting from the sale of your home is also part of the American way of life. Many of us have our nest eggs, our children’s future education needs, or that cruise around the globe tied up in our home’s equity.

How To Avoid A Tax Penalty When Selling Your Home

There are many ways to pay the least amount of taxes when selling your home. Keep in mind that a competent attorney is invaluable in most tax situations. This guide will help you ask the right questions.

The following section of the 1997 tax code changed everything and set the stage for millions of homeowners to profit substantially from the sale of their home, without always having the government's hands in the till.

The Taxpayer Relief Act of 1997 permanently exempted a significant portion of capital gains tax on the sale of a primary residence. According to the code: Single taxpayers, selling their primary residence after May 6, 1997, can exempt up to $250,000 in capital gains. Married couples, filing jointly, can claim up to $500,000. The code goes on to say that a primary residence of the taxpayer must have been owned and occupied for a period of at least two years in a five-year timeframe ending on the date of sale.

Avoiding Tax Penalties

The following will help homeowners avoid substantial tax penalties and determine if they qualify for the capital gains exclusions. This is by no means a complete list. Taxpayers should know their rights, outlined by the IRS.

- A fundamental key to the exclusion is that your home must be your primary residence, as defined by the IRS. The primary residence is the location where you spend most of your time.

- The prospective seller must have owned the home for at least two years in the five years prior to any sale. Couples who are married and filing jointly can use the exclusion when only one qualifies.

- Owning the home is not enough; homeowners must have lived in the residence for two out of five years before it is sold. The 24 months do not have to be a single block of time.

- When looking at future tax benefits. Take full advantage of reinvesting into another like-kind investment property using the proceeds received from the sale of your previous like-kind property using the 1031 exclusion. Investors have 180 days to make another deal on like-kind property.

Do You Have To Buy A House To Avoid The Tax Penalty

The two most impactful exclusions from the 1997 tax code include the five-year rule and the primary home exclusion. To receive either the $250,000/$500,000 exclusion or the homeowners rule, the original homeowner must have lived in the home for two out of the five years prior to selling. The IRS has sneaky ways of checking any statement you make. It is a mistake to think capital gains can be avoided; they cannot, only be deferred.

Consider the 121 loophole when looking to buy another home after a profitable sale. The 121 exclusion would allow a homeowner and the property being held as an investment to exclude capital gains and instead pay depreciation recapture. Only use a well-qualified tax professional when dealing with special situations.

Do I Have To Pay Capital Gains Tax When I Sell My House?

The IRS states, “if a home seller does not qualify or chooses to take the exclusion for $250,000/$500,000, any reported loss or gain from their home must be reported when filing their year-end tax return. If capital gains profits exceed the exclusion, homeowners must report the difference and include that amount as taxable income on their next return.”

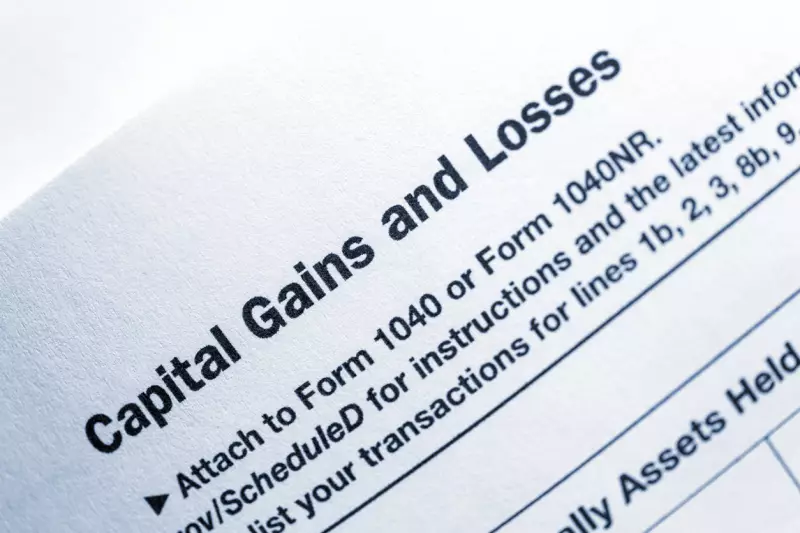

Home properties that are sold within a year are considered short-term capital gains and taxed as ordinary income, which could go as high as 37%. Yowzer! Long-term properties are taxed at no more than 20% and held longer than the one-year threshold. The graduated capital gains tax is a 0%, 15%, or 20% tax rate, based on the homebuyer's taxable income.

2025 Capital Gains Tax

|

Tax rate |

Single |

Married filing jointly |

Married filing separately |

Head of household |

|

0% |

$0 to $48,350 |

$0 to $96,700 |

$0 to $48,350 |

$0 to $64,750 |

|

15% |

$48,351 to $533,400 |

$96,701 to $600,050 |

$48,350 to $300,000 |

$64,751 to $566,700 |

|

20% |

$533,401 or more |

$600,051 or more |

$300,001 or more |

$566,701 or more |

Do You Pay Sales Tax On A House? What You Need To Know

Real estate transactions are unlike the sale of other real property and are generally excluded from sales tax in some states.

Even though excluded, the state levies many other fees and taxes on real estate transactions. Specific transactions, such as construction material purchases or property services, may be subject to sales tax.

Homebuyers and Sellers should be aware of the following fees and taxes associated with a real estate transaction in most states. This list does not apply to all states, and there are plenty of underlying costs that need to be accounted for.

- Stamp Duty is a tax on validating certain legal documents in the transfer of real estate. Around the globe, Stamp Duty has a colorful history; however, in the United States, Stamp Duty is collected by states or counties.

- Property Transfer Tax is a one-time fee imposed by either the county or state when real estate is transferred. The transfer tax is calculated as a percentage of the purchase price or the real value of the property.

- Recording Fees are specific charges levied by the government to record and document mortgages and deeds in all public records. It is the fee to make your transaction public.

- Mortgage Registration Tax is a state-imposed recording fee that some states and counties charge to document a real estate transaction.

States such as Texas rely heavily on property taxes to offset a policy of no individual income taxes. Other states, such as Illinois, impose both higher property taxes and personal income taxes. States use millage and percentages to decide on the amount of tax to be levied.

The average countywide tax charged in 2023 was $1889, with eleven counties charging a paltry $229 annually. Some counties in California and New York have annual property tax bills in excess of $10,000. Five counties in the United States have a tax burden of 2.97%, while the lowest five counties boast a rate of only 0.18%.

Understanding Capital Gains Tax and How It Affects Home Sales

Three factors determine capital gains tax: how long you have held the property, taxable income, and filing status. Capital gains taxes are generally lower than other forms of taxes; however, charges can add up quickly if the home is a large ticket item.

If your home has increased substantially in value, it is never too soon to start planning for a capital gain or loss. Capital gains on real estate are based on the property’s adjusted cost basis, not on what you paid for the home.

Length Of Ownership Matters

Homeowners should understand that long-term gains have a lower tax rate while short-term capital gains are added to taxable income. When deciding on when to sell your primary residence, never forget to account for the time of ownership. Short-term capital rates can be as high as 37%, while long-term rates fall to no higher than 20%.

Exclusions

Several methods exist for homeowners to reduce or limit their capital gains tax. These exclusions can start on the move-in date and carry forward until the property is sold.

- Single Filers $250,000, married filing jointly $500,000

- Hold taxable assets for one day longer than one year

- Take advantage of the 121 exclusion and the 1031 exclusion

- Contribute fully to tax-advantaged 401K and IRA accounts

- Offset capital gains by deducting significant home improvements that add long-term value to the home.

How To Minimize or Avoid Capital Gains Tax When Selling Your Home

It is now the American way to avoid as many taxes as possible, and there are plenty of ways to accomplish the goal if you start early and keep meticulous records.

- Mentioned several times in this content is the primary $250,000/$500,000 exclusion. This avoidance can only be used once every two years and only with the primary residence. (pre-conditions apply)

- Use the 1031 exchange exclusion. Reinvest capital gains from an investment property into a like-kind property.

- Always consider your holding period. Hold taxable assets for longer than one year.

- Make full use of tax-advantaged accounts, including 401K plans, Roth IRA, and 529 accounts.

- Tax-loss harvesting is not for everyone; however, if executed properly, it can help in the battle to minimize capital gains when you have a lot of taxable income. The strategy involves selling non-profitable assets at a loss. (stocks, crypto)

- Consider actively managed mutual funds. Buying and selling assets within the fund invariably creates capital losses, which are passed down to individual investors.

- Inherited assets receive favorable tax treatment from the IRS. The adjusted cost basis for a property is based on the value when the previous owner died, not when they purchased it.

- Charitable giving has always succeeded as a means to minimize capital gains. Charitable tax deductions are long-term line items, and no capital gains tax is assessed on a gain from charitable donations.

Can You Avoid Tax Penalties When Selling Your Home?

If you have owned the home for any day longer than one year, a transaction falls under the long-term capital gains rates, which are substantially lower than the alternative. Just make sure to hasten the qualification rights.

The single most important exclusion for most of us will be the $250,000/$500,000 home deduction, so we must manage that asset with all care.

- The top Short-term marginal rate currently stands at 37%.

- Long-term marginal rate is 20%

- If the capital asset is sold at a loss, taxpayers can use the loss against capital gain.

The IRS is starting to loosen up a bit on how gains and losses are reported and applied to taxpayers' returns, specifically to the sale of the family’s primary asset. However, the IRS's mortgage debt language still lays down the government's basic premise, which is very firm restrictions with compelling deductions.

Some Exclusions and Exceptions

- Each taxpayer must meet all ownership and use tests. In the first five years, the homeowner must have lived in the home for two years. The time does not have to be a single block.

- The IRS has a heart. If you are selling your home due to an unforeseen event, such as a health issue, you may qualify for a reduced exclusion.

- Homeowners who take advantage of the full capital gains exclusions DO NOT need to report the sale of the home on their return.

- Capital losses are deductible and count against the overall Capital gains liability.

- IRS, “Transfer of your home to a spouse or an ex-spouse. Generally, if you transferred your home (or share of a jointly owned home) to a spouse or ex-spouse as part of a divorce settlement, you are considered to have no gain or loss.”

What Is The Tax Penalty For Selling A Home?

A factor to consider when planning your sales and capital gains tax strategies is to make sure you are working with the NET capital and loss numbers. Net gains are taxed at different rates than the taxpayer’s taxable income.

The generous home exclusion covers a lot of planned and unplanned mistakes made by the homeowner. If the life of your home ownership fails to go past two years, try to make the right moves now; we all have health issues, family emergencies, unplanned work obligations, and more that can derail homeownership bliss.

If you sell before the two-year threshold, any capital gain will likely be wiped out with selling fees, and capital gains will be taxed at the homeowner's taxable income rate. Without taking the section 121 home exclusion, taxpayers will need to pay the 8% to 10% in selling fees. Expect to pay realtor commissions, closing costs, and inspection fees.

If homeowners fail to report their home sale correctly, the IRS may see it differently. Any mistake can be added as taxable income and cause the homeowner many problems, such as potential penalties for underreporting income.

There are no special penalties from the federal government solely for selling your home. The only consequence would be underreporting, or you fail to qualify for the exclusion.

Timeframe For Buying A New House To Avoid Tax Penalties After Selling

The Taxpayer Relief Act of 1997 fundamentally changed home sales but also eliminated the antiquated “Rollover Rule.” Before 1997, home sellers had to purchase a new home of equal value within 180 days to defer capital gains.

The Roll Over Rule Is No More

Now, instead of forcing homeowners to buy another home, it is up to the homeowner to decide when they need to sell to take advantage of their capital gains. This IRS section proves there is no mention of any requirement of a rollover rule or anything closely related.

This IRS publication is the definitive guide for selling your home.

IRS-Compliant Reinvestment Strategies

- As mentioned earlier, use a 1031 exchange to reinvest the proceeds of an investment property into another like-kind property. A creative twist is to rent out your primary residence and then use the 1031. (Always consult a property attorney).

- Invest taxable gains into a QOZ (qualified opportunity zone). A QOZ is an economically distressed community where new investments may be eligible for preferential tax treatment.

- Home improvements on a primary residence increase the cost basis while reducing future taxable gains.

Homeowners facing substantial capital gains must meet the two out of five-year residency rule. Carefully document all home improvements with receipts. If the homeowner is considering advanced strategies such as a 1031 exchange, always consult a tax professional.

Tips To Eliminate Or Reduce Tax Penalties On Home Sales

The previous content has attempted to show the many channels and alternative strategies homeowners can use to offset capital gains. However, the most effective means of avoiding penalties is to take advantage of the primary residence exclusion and report income and gains accurately.

- Make absolutely certain you qualify for the primary residence exclusion by living in the home for 2 out of 5 years prior to selling. Use the exclusion once every two years.

- Maximize the cost basis of your home with kitchen upgrades, a new roof, or a garage. Any improvement must add value and prolong the life of the home.

- When selling, do not forget to add realtor commissions, closing costs, and transfer taxes to reduce taxable gains.

- Strategically time the sale to coincide with low-income years so you qualify for the 0% long-term capital gains rate. Avoid selling during high-income years to avoid triggering the 20% tax.

- Offset any gains with capital losses by selling underperforming investments (stocks, crypto). Avoid a wash sale (repurchase the same asset within 30 days)

- If possible, claim an exclusion for special circumstances. (job relocation, divorce, or health issues)

Advanced Strategies

- Convert the home to a rental and use the 1031 exchange. Rent it out for a year to establish the house as an investment.

- Donate the home to a Charitable Remainder Trust, avoid capital gains, and receive income for life. Donate the home directly and eliminate the capital gains.

- Invest gains into a charitable opportunity zone within 180 days of sale.

- Plan for depreciation recapture, or you will owe 25% tax on claimed depreciation.

Start planning at least a year or two before selling your primary residence, and use the many IRS rules and exclusions strategically.

Elena Novak leads real estate research and analysis at PropertyChecker.com, where she digs into housing trends, tracks property data, and unpacks investment strategies across the U.S. With a background in flipping homes and a degree in Business and Real Estate Development, she brings a practical, hands-on approach to market analysis. Elena is especially skilled at uncovering hidden property value and guiding both homeowners and investors through shifting market conditions. She's also passionate about sustainable design and smart home innovation. When she's not analyzing the market, she's probably knee-deep in a DIY project, scouting vintage décor, or building something new in her workshop.

Search Property & Deed Records

Table of Contents

- Avoiding A Tax Penalty

- How To Avoid A Tax Penalty When Selling Your Home

- Avoiding Tax Penalties

- Do You Have To Buy A House To Avoid The Tax Penalty

- Do I Have To Pay Capital Gains Tax When I Sell My House?

- 2025 Capital Gains Tax

- Do You Pay Sales Tax On A House? What You Need To Know

- Understanding Capital Gains Tax and How It Affects Home Sales

- Length Of Ownership Matters

- Exclusions

- How To Minimize or Avoid Capital Gains Tax When Selling Your Home

- Can You Avoid Tax Penalties When Selling Your Home?

- Some Exclusions and Exceptions

- What Is The Tax Penalty For Selling A Home?

- Timeframe For Buying A New House To Avoid Tax Penalties After Selling

- The Roll Over Rule Is No More

- IRS-Compliant Reinvestment Strategies

- Tips To Eliminate Or Reduce Tax Penalties On Home Sales

- Advanced Strategies