What Is a Reconveyance Deed and How Does It Clear Mortgages from Property Records?

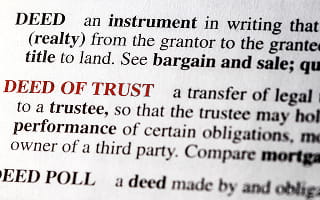

A reconveyance deed is a legal instrument that removes a deed of trust from public records once the mortgage is paid in full, transferring title from the trustee back to the borrower. It proves the lender no longer has a financial interest or lien on the property, ensuring a clear title.

A deed of reconveyance verifies that the property is free of debt encumbrances and confirms that the homeowner has full ownership rights. It is crucial for selling or refinancing; an unrecorded lien can delay a closing, cause buyers to walk away, or prevent new loans. It serves as official documentation that the debt is satisfied, preventing the lender from making potential future claims.

Recording the deed with the county is vital because it officially removes the lien.

What Is a Reconveyance Deed?

A reconveyance deed is a legal document executed by a trustee, acting under a deed of trust, that formally transfers title to the property back to the borrower once the mortgage is paid off. It serves as public proof that the lender's lien has been released and that the title is clear.

The purpose of a reconveyance deed is to formally transfer title to the property from the trustee back to the borrower, confirming that the mortgage is paid in full. It typically involves the trustee (who holds title) releasing it back to the borrower (trustor). Once the lender is paid, they must notify the trustee to initiate the recording of this document in public records. Without this recorded document, the property may still appear to have a lien, which can complicate future sales or refinancing.

Distinction from "Satisfaction of Mortgage"

While both documents prove that a debt is paid off, they are used in different legal systems. The differences are explained below:

-

Reconveyance Deed: Used in states that primarily use deeds of trust (often referred to as title theory states).

-

Satisfaction of Mortgage: Used in states that primarily use mortgages (often referred to as lien theory states).

In essence, a reconveyance deed "reconveys" the title held by a trustee, whereas a satisfaction of mortgage simply clears the lien from the title.

How a Reconveyance Deed Works (Process)

A reconveyance deed formally releases a lender's lien on a property after a mortgage is paid in full. The process involves paying off the loan, notifying the trustee, executing and notarizing documents, and recording them with the county to ensure a clear title, all in accordance with state-mandated deadlines.

The Reconveyance Process Sequence

-

Loan Payoff: The borrower pays off the mortgage loan in full, including any final fees.

-

Lender Notifies Trustee: Within a specified timeframe (e.g., 30 days in many states), the lender notifies the trustee that the loan is satisfied and requests a reconveyance.

-

Trustee Prepares & Executes Reconveyance: The trustee (usually a title or escrow company) prepares the "Full Reconveyance" document, which affirms that the debt is cleared.

-

Notarization: The trustee signs the document, and the signature is notarized to make it legally binding.

-

Recording in County Records: The trustee records the notarized deed with the local county recorder's office. This crucial final step officially removes the lien from the public record.

Statutory Deadlines and Considerations

-

Timeframes: State laws vary; for instance, California law requires trustees to record the reconveyance within 21 calendar days of receiving the necessary documents.

-

Delays: The process can take up to two months, depending on the lender and state regulations.

-

Responsibility: While lenders are responsible for initiating the process, borrowers should ensure they receive a copy of the recorded document to confirm that the lien has been removed.

Who Needs to Sign a Deed of Reconveyance?

A deed of reconveyance must be signed by the trustee (the third party holding title) or, in some cases, by the lender (the beneficiary) to officially document that the mortgage has been paid in full and the lien is removed. This signature must be notarized to be legally valid for filing with the county recorder's office.

The Parties Involved

-

Trustee: The trustee named in the original Deed of Trust is responsible for signing the document to officially transfer title back to the borrower.

-

Notary Public: The trustee's signature must be notarized, and in some states, additional witnesses may be required.

-

Lender: While the trustee often signs, the lender (beneficiary) may also be involved in authorizing the reconveyance.

The borrower usually does not need to sign a deed of reconveyance, as it is released to them rather than by them.

Deed of Reconveyance Form

A deed of reconveyance form is a legal document that acts as public proof that the trustee has transferred title back to the borrower, officially clearing the property title.

Components of a Deed of Reconveyance Form

-

Borrower and Lender Information: Names and addresses of the trustor (homeowner) and beneficiary (lender).

-

Trustee Information: Name of the trustee authorized to release the lien.

-

Original Deed of Trust Reference: Recording details (book/page or instrument number) of the original deed.

-

Property Legal Description: Precise legal description and parcel number.

-

Statement of Debt Satisfaction: A statement confirming that the loan is paid in full, often including a request to reconvey.

-

Signatures & Notarization: Signed by the trustee and notarized.

Where to Obtain the Form

-

Lender/Trustee: Usually initiated by the lender/servicer upon payoff.

-

County Recorder Office: Local county clerk websites often provide forms.

-

Title Companies: Title companies involved in the transaction.

-

Online Legal Resources: Online legal document services.

To prevent rejection by the county recorder, accuracy is crucial. Mistakes in the legal description or recording references can delay the removal of the lien, causing issues when trying to sell or refinance the home. Deeds of reconveyance are primarily used in "deed of trust" states, while "mortgage" states use a Satisfaction of Mortgage.

Reconveyance Deed vs. Satisfaction of Mortgage

A reconveyance deed clears title for a paid-off Deed of Trust (3-party system), whereas a Satisfaction of Mortgage releases a paid-off Mortgage (2-party system). Reconveyance involves a trustee transferring legal title back to the borrower, while satisfaction involves the lender releasing the lien directly. This distinction matters for accuracy in clearing liens.

Comparison: Reconveyance Deed vs. Satisfaction of Mortgage

-

Document Type:

-

Reconveyance Deed: Used in a Trust Deed to officially transfer title from the trustee back to the borrower.

-

Satisfaction of Mortgage: Used in mortgage states to formally record that the borrower's debt is paid in full.

-

Parties Involved (Reconveyance): Trustor (borrower), Beneficiary (lender), and Trustee (third-party holding title).

-

Parties Involved (Satisfaction): Mortgagor (borrower) and Mortgagee (lender).

-

-

Key Action:

-

Trustee in Reconveyance: The trustee executes and records the deed, thereby clearing title after the beneficiary confirms the payoff.

-

Lender in Satisfaction: The lender (mortgagee) signs and records the document.

-

State Usage: Deeds of Trust (e.g., CA, NV, TX) typically involve reconveyances. Mortgage states (e.g., FL, OH) use Satisfactions.

-

Why the Distinction Matters

-

For Title Examiners: It is crucial to verify that the correct entity (trustee vs. lender) released the lien. A recorded reconveyance deed is required to remove the lien in a deed-of-trust state, whereas a satisfaction is required in other states.

-

For Attorneys: Failure to record a reconveyance can leave a "cloud on title" (an active lien) even after the debt is paid. If a trustee has gone out of business, obtaining a reconveyance can be complex.

-

Foreclosure Process: Deeds of trust generally allow for non-judicial foreclosure (faster), while mortgages often require judicial foreclosure (through courts).

The core difference is that a reconveyance fixes a three-party security structure (the trustee holds title), while a satisfaction fixes a two-party structure (the lender holds the lien).

Recording & Public Notice Requirements

Recording a deed of reconveyance is essential to legally prove that a mortgage is paid off, provide constructive notice to the public, clear the property title, and ensure the property's marketability. Unrecorded releases create "clouds on title," causing severe refinancing delays, title insurance issues, and potential litigation. Often, they require legal action to prove ownership.

Why It's Important to Record the Reconveyance Deed

-

Constructive Notice: Recording in county records notifies the world, including future buyers and creditors, that the prior lender's lien has been extinguished.

-

Clearing Title & Marketability: It formally clears the title, removing the encumbrance, which is necessary for a "clear title" needed for resale.

-

Priority & Protection: It establishes a permanent, public, chronological record of the transaction, protecting the homeowner against future claims.

-

Refinance/Closing: Title companies require recorded evidence of previous loan satisfaction to issue title insurance for new loans or sales.

Risks of Delays or Unrecorded Releases

-

Clouds on Title: The public record still shows a lien, which makes the property appear to have outstanding debt.

-

Refinance/Sale Delays: Buyers or lenders may delay proceeding until the title is officially clear.

-

Legal/Financial Headaches: If the lender fails to record the reconveyance, the homeowner may need to take legal action or file the reconveyance manually to clear title.

-

Priority Disputes: Unrecorded interests may lose priority to subsequent, properly recorded interests, depending on state law.

Role of Trustee, Lender, and Borrower

A reconveyance formally removes a mortgage lien after full repayment, with the trustee executing the document, the lender initiating the request, and the borrower confirming its recording to clear the title. Failure to record in a timely manner can result in statutory penalties for the lender and significant title issues for the borrower.

Roles in the Reconveyance Process

-

Borrower: Pays the loan in full and should verify that the trustee or lender has recorded the reconveyance with the county recorder to clear the title.

-

Lender (Beneficiary): Upon receiving final payment, the lender must notify the trustee and instruct them to prepare and record the deed of reconveyance.

-

Trustee: The neutral third-party holding title in trust, responsible for executing, signing, and recording the reconveyance document upon the lender's instructions.

Statutory Duties and Timeline

-

Timing: Lenders and trustees are required to record the deed of reconveyance within a specific period, often 21 days after receiving the payoff in some jurisdictions (e.g., California), or within 60-90 days in others.

-

Documentation: The trustee must record the full reconveyance in the county recorder's office where the original deed of trust was filed.

Issues with Delaying and Borrower Remedies

-

Lender/Trustee Liability: If the reconveyance is not timely delivered or recorded, the lender may be liable for statutory penalties, damages, and legal costs.

-

Borrower Remedies: Borrowers may bring lawsuits against lenders for damages caused by the delay, such as the inability to sell or refinance the property.

-

Title Issues: If not recorded, a lien remains on the public record, causing "clouds" on the title that can derail future transactions.

Title Insurance & Future Transactions

Title companies require a recorded deed of reconveyance to prove a mortgage is paid, ensuring the new buyer or lender holds a first-priority lien. Unreleased trust deeds appear as title exceptions because, without a public record of satisfaction, they constitute a legal encumbrance. A recorded reconveyance clears this by officially removing the lender's claim.

Why Unreleased Trust Deeds Appear as Exceptions

-

Constructive Notice: The public record does not show the loan was paid off, implying the lien still exists.

-

Security Interests: A deed of trust transfers title to a trustee; a recorded release is required to return full ownership.

-

Marketable Title: Unreleased liens create uncertainty about ownership, preventing the transfer of a clean title.

How Reconveyance Cures the Exception

-

Official Release: The trustee records the deed of reconveyance in county records, officially removing the security interest.

-

Clears the Chain of Title: It acts as proof of satisfaction, allowing the title company to remove the exception from the final policy.

-

Removes Risk: The recorded document confirms the property is no longer used as collateral, protecting future transactions.

Without this, the lender could theoretically attempt to foreclose on a paid-off loan, which is why insurers mandate its recording.

Risks, Pitfalls & How to Avoid Them

Some pitfalls with reconveyance deeds include lender delays, trustee backlogs, incorrect legal descriptions, and unrecorded documents. Avoid these by confirming the recording, using escrow holdbacks, and obtaining payoff letters.

Risks and Pitfalls

-

Lender/Trustee Delays: Lenders may take weeks or months to send release instructions to the trustee, or trustees may have backlogs, leaving the lien active on public records even when it is paid off.

-

Misapplied Payoff Funds: Payments might not be properly credited, preventing the initiation of the reconveyance process.

-

Incorrect Legal Descriptions: Typos in the legal description, owner names, or loan details can render the deed invalid or ineffective.

-

Unrecorded Reconveyance: The deed is signed but not officially recorded with the county, which is necessary to publicly clear the title.

-

Lost Documents: If the original deed of trust is lost and a reconveyance cannot be produced, you may need to secure a costly bond to clear the title.

How to Avoid Issues (Strategies)

-

Proactive Borrower Follow-Up: Do not assume the process is automatic. Request a copy of the recorded deed of reconveyance from your lender or the county recorder's office shortly after payoff.

-

Use Escrow Holdbacks: During a sale, ensure the escrow company holds funds to guarantee the lender releases the lien, which provides incentive for swift action.

-

Verify Payoff Letters: Obtain a formal payoff letter to ensure the exact amount is paid, reducing the risk of misapplied funds.

-

Check for Accuracy: Thoroughly review the deed to ensure the property descriptions, names, and recording information are correct.

-

Contact Lender Immediately: If a reconveyance is not received within a reasonable timeframe (typically 30-60 days), contact the lender's payoff department immediately.

State-Specific Variations

Reconveyance deed requirements vary significantly. State-specific laws dictate the process, with some states imposing strict timelines and penalties on lenders for failing to record the release. Terminology also varies, for example, "Full Reconveyance" or "Satisfaction of Mortgage".

State-Specific Variations and Legal Requirements

-

Terminology: While "Deed of Reconveyance" is common in trust deed states, other terms may include "Release of Deed of Trust" or "Satisfaction of Mortgage".

-

Strict Timelines: Many states, such as California, impose strict, short deadlines for the trustee to record the reconveyance after the loan is paid.

-

Penalties: Failure to record the deed in a timely manner can result in significant legal and financial penalties for the lender.

-

Process Differences: Some states require the lender to handle the recording, while others may require the borrower to ensure it is filed with the county recorder.

It is essential to check state-specific laws, as procedures vary significantly regarding who records the document and the timeline involved. Borrowers should ensure they receive a copy of the recorded deed to confirm the lien is officially removed from their title.

Check First with PropertyChecker

Reaching the final mortgage payment is a huge milestone for many homeowners, but securing a reconveyance deed is the essential final step to guarantee a clean, marketable title and to formally remove liens from public records.

While lenders and trustees are responsible for compliance when filing this document, as the borrower, you must be vigilant to avoid future, costly title disputes. Do not leave your home's clean title to chance; verify that your reconveyance is properly filed to truly own your property free and clear.

PropertyChecker can help with due diligence. We provide robust property records that allow you to quickly and easily find information about a specific property. Review things like ownership history, deeds, liens, foreclosures, loans, building permits, and much more. Check PropertyChecker to see whether the proper reconveyance deed has been filed.

Table of Contents

- What Is a Reconveyance Deed and How Does It Clear Mortgages from Property Records?

- What Is a Reconveyance Deed?

- How a Reconveyance Deed Works (Process)

- Deed of Reconveyance Form

- Reconveyance Deed vs. Satisfaction of Mortgage

- Recording & Public Notice Requirements

- Role of Trustee, Lender, and Borrower

- Title Insurance & Future Transactions

- Risks, Pitfalls & How to Avoid Them

- State-Specific Variations

- Check First with PropertyChecker

Table of Contents

- What Is a Reconveyance Deed and How Does It Clear Mortgages from Property Records?

- What Is a Reconveyance Deed?

- How a Reconveyance Deed Works (Process)

- Deed of Reconveyance Form

- Reconveyance Deed vs. Satisfaction of Mortgage

- Recording & Public Notice Requirements

- Role of Trustee, Lender, and Borrower

- Title Insurance & Future Transactions

- Risks, Pitfalls & How to Avoid Them

- State-Specific Variations

- Check First with PropertyChecker

Investors Properties Resources

- How to Buy Probate Real Estate Properties

- How to Find Investment Properties

- How to Profit from Fixer Upper Homes

- What Is a Deed-in-Lieu of Foreclosure

- Government and Seized Property Auctions

- How Property Auctions Work

- How to Buy Bank-Owned Properties

- How to Buy Tax Lien Properties

- How to Choose a Property Investment Company

- How to Finance an Investment Property

- How to Find and Buy FSBO Homes

- How to Find Investment Properties

- How to Find Off-Market Properties

- How to Find Vacant Homes in the US

- What Is a Cloud on Title

- How to Wholesale Real Estate

- Restrictive Covenants and Deed Restrictions

- Types of Warranty Deeds

- What Are Easements

- What Are Encumbrances in Real Estate

- What Are HOA Liens

- What Are Real Estate Investment Trusts

- What Are REO Properties

- How to Find Tax Delinquent Properties

- What Are UCC Liens

- What Is a Bargain and Sale Deed

- What Is a Judgment Lien

- What Is a Lis Pendens

- What Is a Mechanic's Lien

- What Is a Quiet Title Action

- What Is a Quitclaim Deed

- What Is a Short Sale in Real Estate

- What Is a Special Warranty Deed

- What Is a Statutory Warranty Deed

- What Is Adverse Possession

- What Is Skip Tracing in Real Estate

- How to Use the BRRRR Method

- What Is Vacant Home Insurance